CHIPS Act: The Climate Consequences of a Growing Demand for Semiconductors

An exploration of the climate and environmental consequences of onshoring semiconductor manufacturing

Last week, we covered the trillion-dollar policy push by Europe and the United States. Today, we dive deep into the CHIPS Act in the United States and its implications for onshore manufacturing, AI, and clean energy.

But first, here’s the best climate company and job we've heard of:

Climate Company: Despite a slowdown in venture capital this year, infrastructure funds raised a whopping $9B and there are no signs of stopping. Orennia is poised to become the data player for these players with its unique analytics and datasets on the solar, wind, storage, power, RNG, CCUS, clean fuels, and hydrogen sectors. They raised a Series B last November from Wellington Management.

Cool Climate Job: Prelude Ventures, a storied early stage climate VC fund that started in 2009, is hiring a pre-MBA associate in SF, CA. The fund invested early in companies such as AMP Robotics (Series C), Boston Metal (Series C), and Fervo Energy (raised another $244M this Feb). More info is here.

Introduction

The acceleration of genAI, the electrification of transportation, and the ever-growing demand for electronics can only mean one thing — we will need more chips. By 2030, McKinsey predicts the semiconductor industry will grow to over $1 trillion in revenue, with 70% of the growth driven by automotive, computation and data storage, and wireless.

At the same time, the U.S. is trying to move manufacturing out of East Asia and onto U.S. soil after a shortage in semiconductor supply in 2021. The U.S. swiftly allocated $50B+ to the CHIPS and Science (“CHIPS”) Act which will onshore the semiconductor supply chain, threatening our climate emission reduction goals and water security (more on this later!). On the other hand, the CHIPS Act could unlock $67B+ toward the research and development of zero-carbon industries, if agencies continue to allocate the same percentage of their current funding to climate research. The tug of war between these two themes of the CHIPS Act will make or break the climate implications over time.

The CHIPS Act

The CHIPS and Science Act established funding for investments ranging from specific national security projects to grants that increase the capacity of semiconductor manufacturing plants (“fabs”) operating domestically. Over the last six months, the dollars have begun to roll out. In December 2023, BAE Systems bagged the first award. Recent grants were awarded to legacy Taiwanese and Korean chip manufacturers, Samsung and TSMC, for expanding their U.S.-based fabs in the southwestern United States.

A Simplified Look at the Semiconductor Value Chain

At its most basic level, the value chain for semiconductors can be broken down into:

1) Chip Design or work firms like Nvidia and Qualcomm: develop the blueprints for production

2) Chip inputs: supply chain of raw materials, equipment, and other inputs needed for production of chips

3) Chip Manufacturing: where players like TSMC take those inputs and designs to bring chips to life

4) Chip Applications or the final step: when chips are deployed across use cases spanning automotive, personal devices, computing, and more

While the climate implications across the detailed value chain of chips are large, we have our eyes on the following:

A) manufacturing at fabs where much of the CHIPS Act is allocating dollars to and B) the downstream impacts from certain applications (e.g., advanced microchips being deployed for AI and the energy implications of the rising demand for computing).

The Negative Climate and Water Impact of the Semiconductor Industry

Estimates of yearly GHG emissions have put the semiconductor manufacturing industry at upwards of 75 Mt of CO2e across Scope 1 + Scope 2, split into 30 Mt and 45 Mt respectively. A broader look at upstream Scope 3 emissions would dramatically increase this number.

Here is where we are concerned:

Energy Use: The energy required to run the fabs is one of the largest emissions levers. At TSMC alone, 62% of the firm’s emissions were tied to energy needs. McKinsey estimates that some large fabs can outpace automotive plants and oil refineries on power usage, with upwards of 100 MWh used per hour. Given this large energy demand, chip manufacturers are looking to renewables. Both Intel and TSMC have made commitments to 100% renewable energy by 2030 and 2050, respectively. However, the intermittency of renewables poses a major challenge to the industry’s climate goals. Like any manufacturing plant, fabs rely on a constant draw of baseload power from the grid, which is typically produced by natural gas or coal.

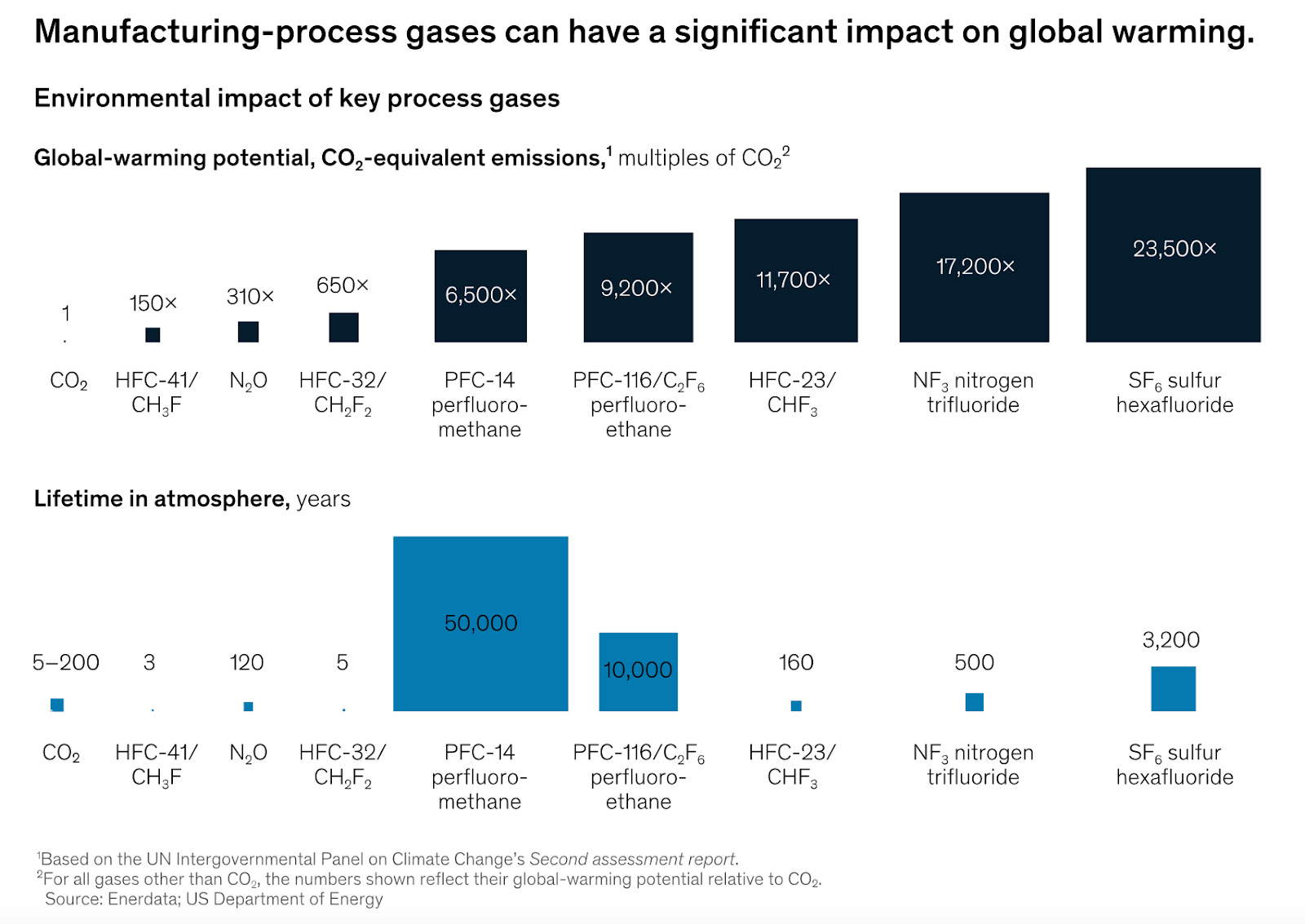

Process Gases: A less obvious driver of emissions is the process gases required in the manufacturing of chips. These gases like perfluorocarbons, hydrofluorocarbons, and others, help with a range of processes, from etching on wafers to the cleaning of tools. These have high global warming potential if released into the atmosphere and the semiconductor community is working to lessen their emissions impact. In 2023, the World Semiconductor Council committed to emissions reduction goals from perfluorinated compounds (PFCs) by 2030. Companies like Solvay and Air Liquide are innovating to help reduce the global warming potential of these gases and processes.

Source: McKinsey

Water: Like with many industries, water plays a critical role in the semiconductor space with fabs consuming millions of gallons a day. The TSMC expansion in Arizona has the state on edge around its water supply and Taiwanese chip production water usage came into conflict with farmers’ needs. Manufacturers, however, acknowledge the issue and are actively working to implement new water resource management processes to address it. TSMC themselves achieved a water recycling rate of upwards of 85% in 2019.

PFAs (“forever chemicals”): PFAs are tiny synthetic chemicals like fluoropolymers that, once produced, exist forever in our environment. These chemicals end up in public water systems and lead to a litany of health issues, including cancer. Litigation over their effects is building, and regulators are increasingly cracking down on their production for a variety of products like nonstick pans, stain-resistant upholstery, firefighting foam — and semiconductor production. In a letter to the EPA, the microelectronics trade group SEMI said that tightened oversight on PFAs “would significantly hamper the domestic semiconductor industry despite the expressed goals of the Administration to the contrary and the detriment of the U.S. economy.”

Downstream Impact: Chips in Data Centers + AI Climate Impact

Semiconductors are the building blocks of nearly all electronic devices, and recently, improvements in semiconductor technology and manufacturing have underpinned the advancements we’ve seen in artificial intelligence. The rise in AI demands a massive energy burden from these chips that drive servers in data centers around the world. One study estimates that data centers accounted for 126 Mt CO2e in 2020. Just two years later, the yearly electricity consumption for global data centers spiked to 240-340 TWh of electricity – or roughly the energy consumption of California.

A range of players are working to address the climate impact from data centers. To lessen the burden on the grid and carbon-intensive power sources, big tech companies like Microsoft and Google are exploring SMRs (small modular nuclear reactors) and nuclear’s ability to address electricity planning and compute needs (above and beyond the large investments they’ve made toward renewables already). Startups are tackling different pieces of the problem as well. Crusoe, for example, is addressing the problem with a unique approach taking gas that would have been flared into the atmosphere and converting it to power modular data centers. Outside of energy generation, start-ups like JetCool and LiquidStack are developing different forms of liquid cooling to address the fact that 30–40% of data centers’ energy is used for cooling.

Our Takeaways

Investments in the semiconductor industry can advance our progress on climate goals, whether it be through better AI-drive climate models or supporting the shift from internal combustion engines to electric vehicles. However, the manufacturing of the underlying chips, along with the increased energy demands of downstream applications, present significant climate impacts that cannot be ignored.

Without a clean source of baseload power, renewable water practices, and the use of PFA alternatives, the CHIPS Act, on its face, is not a climate or environment bill. The CHIPS Act is at a tipping point between catalyzing a water- and carbon-intensive semiconductor industry in the United States and accelerating climate innovation to decarbonize. We need innovators, policymakers, and corporate net zero corporate teams on board to ensure that the policy is net carbon emission positive.

Author Bios

Georgia is an MBA candidate at Stanford Business School. Before Stanford, she worked in sustainable agriculture investing and clean energy investment banking. She recently traveled to Taiwan and South Korea with classmates to meet with major semiconductor supply chain players, including TSMC and Samsung.

Zac is a joint MBA/MS candidate at Stanford’s Graduate School of Business and Doerr School of Sustainability. Before Stanford, he worked in corporate strategy & development at an edtech firm in Washington, DC. One area of his interest is in the public-private sector coordination needed to fund the transition to a net-zero economy.

Nice article -- This highlights an oft-overlooked side of the IRA/BIL/CHIPs legislation: the climate implications for expansion/greenfield development of the domestic semi-conductor industry. From what's discussed in this article, it seems like the relative climate impact of onshoring production will boil down to who can clean up their grid faster, the US or China?