Decoding: Carbon Accounting

In The Gigaton, we profile companies working on solutions with a gigaton impact. In the first installment of our new series - Decoding - we turn our attention to large corporations that set Net Zero targets and publish sustainability reports. Even though many do not directly work on climate, they are still important contributors to global decarbonization. By working to reduce their carbon footprints to Net Zero, many are providing much-needed demand for clean products and services.

But what does “Net Zero” exactly mean? When they say Scope 1, 2, and 3 emissions, what does that actually cover? How does one even measure an emission factor? Who is responsible for the calculation and reporting of these measurements?

This week, we get “meta” and dig into these questions in this article with help from Abigail Mathieson, a Research Fellow at Stanford’s Precourt Institute for Energy. We hope this is a good primer to get you up to speed on Net Zero and the work of Carbon Accountants.

“Net Zero”: The Trend and The Opportunity

“What gets measured gets managed.” This maxim, a foundational piece of business wisdom, has finally reached the climate movement. More than 70 countries and 3,000 businesses and financial institutions have set Net-Zero targets for their greenhouse gas emissions. These voluntary pledges have received considerable attention, as they cover over 76% of current global GHG emissions. If achieved, net-zero pledges could translate to rapid decarbonization of our global economy.

Major governmental bodies in the UK, EU, and the United States have begun to announce regulations around carbon disclosures over the past few years. To date, the most impactful carbon footprinting regulation is the EU’s CSRD (Corporate Sustainability Reporting Directive), which mandates large and SME companies disclose their Scope 1, 2, and 3 emissions; the estimated number of companies impacted is 50,000. Companies must apply the rules in 2024 for reports published in 2025.

Why carbon?

The climate community has focused on one of the most urgent and critical climate change indicators: greenhouse gas emissions (“GHG”). There are many greenhouse gases, all with different levels of atmospheric duration, chemical structure, and anthropogenic emission sources. To simplify measurement, all of these gases (NOx, SOx, NH4, CH4, etc) are converted into a carbon dioxide equivalent, referred to as CO2e. While, in many ways, tracking CO2e is an oversimplification of the complexities of our physical climate systems, it also serves as a high-impact, harmonizing metric to track and reduce.

How do people “account” for carbon emissions?

Right now, most companies calculate their GHG emissions using an emissions factor, “a representative value that attempts to relate the quantity of a pollutant released to the atmosphere with an activity associated with the release of that pollutant.” This factor is a substitute for primary data. Primary data would be collected by a CO2 monitor in the tailpipe of the car, or in the smokestacks of a factory.

Primary data on emissions is often challenging and expensive to obtain, so secondary data and data averages are accepted by most reporting frameworks in use today. For example, 1 kWh of electricity used generates (on average) 0.5 kg of CO2. A company would sum up all the kWh of electricity it used in a year and multiply that by 0.5 kg of CO2.

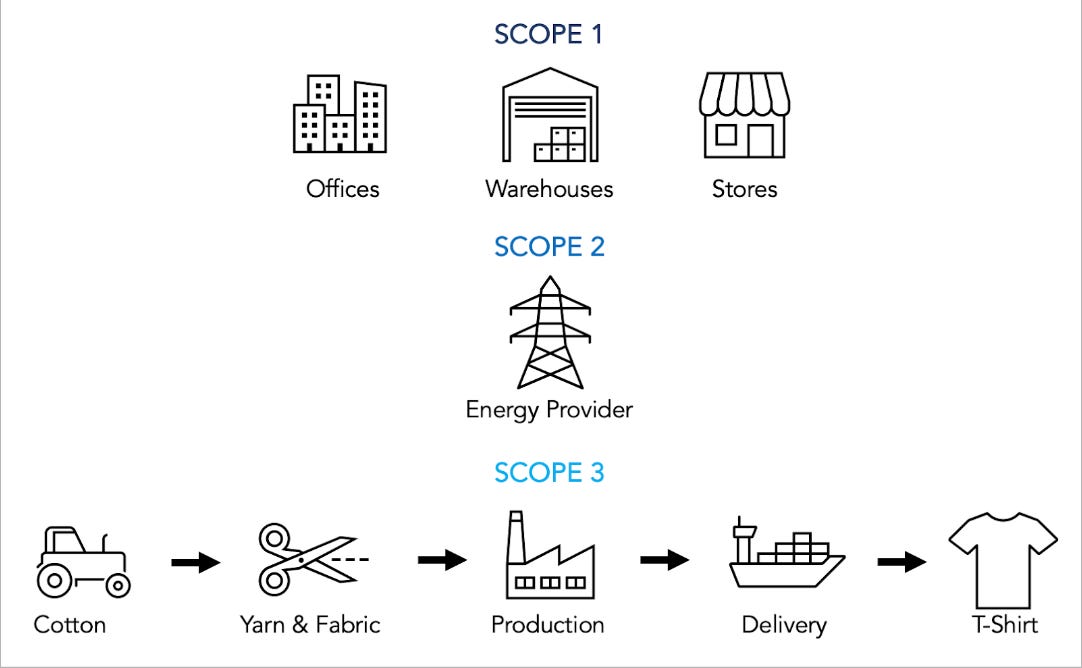

What are Scope 1, 2, and 3 emissions?

The prevailing carbon accounting system used by companies today is the Greenhouse Gas Protocol (GHGRP). The World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD) launched the GHGP Corporate Reporting Standard in 2001, and since then, at least 85% of reporting companies have adopted their methodology. The GHGP categorizes a company’s emissions under three “Scopes”:

Scope 1: GHG emissions from sources that are owned or controlled by the company, such as the gasoline used to power a company-owned delivery vehicle.

Scope 2: GHG emissions from the upstream collection, transportation, and combustion of fossil fuels used to generate electricity used by the company.

Scope 3: Indirect GHG emissions that occur as a consequence of a company’s activities, but from sources not owned or controlled by the company. For instance, the upstream emissions from mining, transporting, and processing raw materials, or the downstream electricity used to charge your cell phone or dry your socks.

Image 1: Example of a simplified corporate GHG inventory: Scope 1, Scope 2, and Upstream Scope 3 (“cradle-to-gate”). Downstream Scope 3 (gate-to-grave) is not shown.

What are the challenges with this system?

The GHG Protocol and the concept of emissions “Scopes'' were originally created as a risk management tool; global carbon pricing was perceived as imminent, and companies needed visibility into their financial risk. Twenty years on, this same system persists. Unfortunately, many key features of GHGP’s carbon risk management tool become fatal flaws as they are stretched and leveraged for carbon accounting. As global markets continue to lean on the GHGP, we need to recognize and address these issues and encourage a systems shift toward true accounting.

Carbon inventory boundaries are flexible under the GHGP framework. This was great for risk management (each company can tailor their view to their needs), but it is bad for accounting. Flexible boundaries allow users to game the system, and greatly limit comparability across companies: emissions can be pushed out of a corporate inventory or divested.

Market-based trading mechanisms (currently used in Scope 2 accounting, but recently proposed for expansion into Scope 3) permit users to purchase “credit” for reductions without actually investing in or delivering decarbonization. Purchasing a Scope 2 Renewable Electricity Certificate (“REC”) allows a company's inventory to reach Net Zero but does little for national or global emissions or Net Zero targets.

The GHGRP allows the use of emissions intensities or averages. This creates a “free rider” problem for companies seeking to reduce emissions. Let’s say Company A uses the industry average method to calculate its emissions from cotton production. Other companies buying cotton from that region will show the same emissions figures on a normalized basis. Company A then decides to decarbonize its cotton production, investing time and capital in working with producers to utilize a new tilling process that reduces anthropogenic emissions by 25%. Over the next few years, cotton production emission factors in that region dropped by 5% due to Company A’s decarbonization actions. So company A records a 25% reduction, but all other companies in the region get to record a 5% reduction, even if they aren’t using the sustainably produced cotton or investing in decarbonization.

Scope 3 is often the greatest driver of a company’s emissions (up to 50%+), but it is a largely estimated and/or optional category according to the GHGP. This opens the door to greenwashing—a company can set narrow boundaries to improve its emissions intensity, or cherry-pick the emissions that it can easily reduce—but such judgment calls are also necessary because of the enormous complexity of accurately measuring and tracking Scope 3.

An ideal system would be accurate, consistent, comparable, auditable, and trackable over time; a roadmap for countries, corporations, and communities, to decarbonize our atmosphere.

In our next edition, we will dive into the companies working on these challenges and share our thesis on this space. Stay tuned!

If you are interested in diving deeper into these carbon accounting topics, please check out Stanford’s Sustainable Finance Initiative and their recent Reuters Op Ed.

Well done. The next, most critical step is adding cost. For more on this read Accountability: Why We Need to Count Social and Environmental Cost for A Livable Future (June 2023). The definition of ACCOUNTABILITY in Merriam Webster: A willingness to accept responsibility and account for one’s actions. In a recent year P&G scope 1&2 emissions were 4.1 mt and scope 3 reached 248.4. At $150 ton scope 1-3 has a climate change costs of $37.8 billion almost equal to the companies net profit of $39 billion.