Uncovering Distributed Solar

By Katherine Playfair and Juan Saez

Gigaton Potential

Distributed solar photovoltaics (PVs) have the potential to avoid 27-69 gigatons of greenhouse gas emissions by 2050 — about 3-4% of required emissions reductions - thanks to up to a 55x rise(!!) in global electricity generated from this renewable source between 2020 and 2050. The large range can be attributed to some of the usual suspects surrounding policy, financing, and market development. With implementation costs reducing by the day, distributed PV technology could save $7.9-13.5tn in associated operation, maintenance, and fuel costs across its lifetime.

You Might Be Interested If...

You want to work on the headline pathways to net-zero

You crave a bit less long-term uncertainty with clear momentum on both the technology and commercial fronts

You still desire room to enable critical improvements that could exponentially improve the economics of a net-zero pathway, develop market systems, and remove barriers to mass scale

You are passionate about decarbonizing growth in emerging economies

Solution Summary

Before beginning, it’s important to highlight that today’s newsletter covers distributed solar, and not utility-scale. In general, distributed generation involves smaller projects that generate and consume energy for end-users, such as residential homeowners or corporations, while utility-scale generation features bigger projects that generate and sell electricity to wholesale buyers. Check out this article from Green Tech Media for more information on how the two methods differ, despite both being required to decarbonize our economy.

Photovoltaic (PV) panels use thin wafers of silicon crystal to generate energy. As photons strike them, they knock electrons loose and produce an electrical circuit. These subatomic particles are the only moving parts in a solar panel, which requires no fuel and produces clean energy.

The installation of small-scale solar systems and utility-scale systems has skyrocketed over the past decade. Technological advances (e.g., 2nd and 3rd generation solar cells that are denser and/or made of alternatives to silicon), system-level improvements such as aggressive government incentives and innovative financing mechanisms, and retail market reforms (e.g., net metering) have driven cost reductions. However, these tailwinds have mostly driven adoption in China, the US, and Europe. India and most other emerging economies are falling behind due to insufficient policy-based incentives and sources of financing.

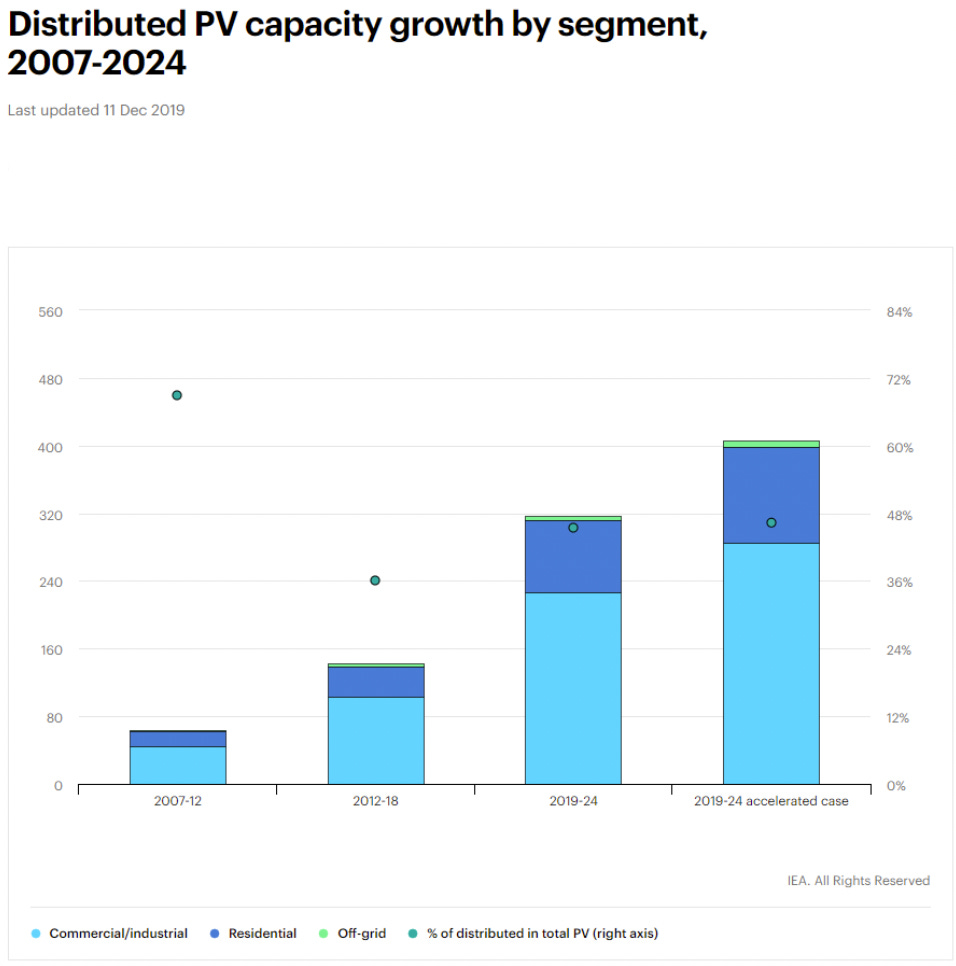

Commercial and industrial property make up >60% of the projected demand for distributed solar power by 2024 and will continue to drive growth moving forward. However, the residential market continues to grow rapidly as well, and significant market reforms, especially around net metering (in which solar energy owners, such as homeowners, are credited for the electricity they add to the grid), are mostly in the residential space.

The future is promising. The combined advances in PV and battery technologies will continue to make the economics of distributed solar PV systems attractive independent of policy incentives and combat the big issue of intermittency. As distributed solar becomes increasingly competitive with fossil fuels and green financing for developing countries rises, these countries should be able to leapfrog fossil fuels straight to renewable energy.

Distributed solar must be part of any toolkit to provide clean energy for development. In grid-connected areas, rooftop panels can put electricity production in the hands of households. In rural areas, distributed solar can accelerate access to affordable, clean electricity, becoming a powerful tool for eliminating poverty.

Key Players

The distributed solar PV market is highly fragmented along the value chain, with only a few players integrating such as First Solar and Juwi Solar across key steps. Most of the consolidation occurs in panel manufacturing.

The key steps in the value chain are

1) Manufacturers of cells, wafers, panels, and modules: Jinko Solar and Trina Solar

2) Project developers who build the projects: Next ERA and other regional players

2) Operating and maintenance companies: First Solar and SOLV

As distributed solar becomes an increasingly global solution, we may see a few players emerge with economies of scale and integration advantages.

Opportunities for Innovation

Solutions for intermittency. How can we ensure 24/7 electricity while primarily depending on distributed solar PV systems? These systems must rely either on alternative backup sources (e.g., fossil fuels, geothermal, nuclear) or long-duration storage systems.

More effective panels. The industry is already at work developing 2nd and 3rd-generation solar cells, working towards denser cells and alternative materials.

Manufacturing and installation. Economies of scale and related efficiencies could be integral to further economic improvements.

Retail market reforms. Net metering can offer great incentives for homeowners to take on residential solar, which currently has challenging breakeven timescales (5-20 years depending on where you live!).

Regulatory and financing innovation. To continue the accelerating growth of the segment, tax credits, project financing, and other mechanisms have to continue evolving in order to meet the unique needs of system builders and individual commercial, industrial, and residential system customers

Sources

https://drawdown.org/solutions/distributed-solar-photovoltaics

https://www.sciencedirect.com/science/article/pii/S0038092X20309993

https://www.statista.com/statistics/858456/global-companies-for-pv-cell-and-module-shipments/

https://www.technavio.com/report/solar-pv-balance-of-systems-market-industry-analysis